If you own a home in Central Florida, a wind mitigation inspection might be one of the most financially useful things you can do this year. Florida homeowners already deal with some of the highest insurance premiums in the country, and a wind mitigation inspection is one of the few tools that can actually bring those costs down.

Under Florida law, insurers are required to offer discounts to homeowners with verified wind-resistant features. A wind mitigation report is how you prove your home qualifies.

Here’s what a wind mitigation inspection covers, what inspectors look for, and why it matters whether you’re buying, selling, or just trying to lower your annual insurance bill.

What Is a Wind Mitigation Inspection?

A wind mitigation inspection is a focused assessment of a home’s construction features to determine how well it can hold up in hurricane-force winds.

This kind of inspection doesn’t cover every system in your house. The entire focus is on the structural and protective elements that affect how your home performs in a major wind event.

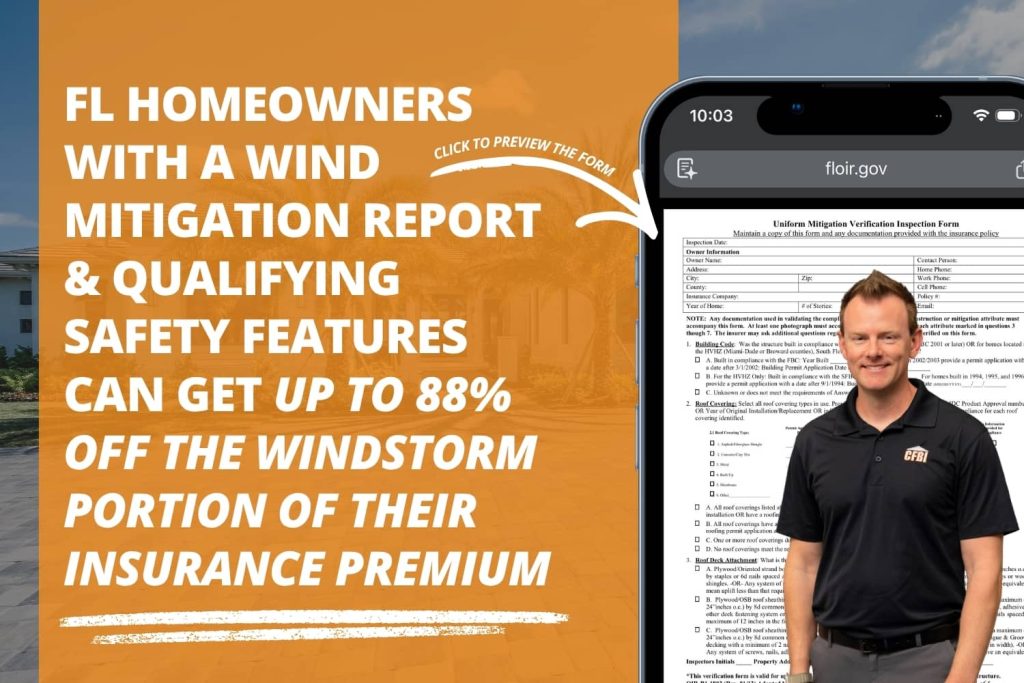

The results are captured on a standardized state form called the OIR-B1-1802, also known as the Uniform Mitigation Verification Inspection Form. Once complete, that form goes to your insurance carrier, who uses it to calculate any applicable discounts on your policy. The report is valid for up to five years, as long as no major changes are made to the structure.

This is not the same as a 4-point inspection. A 4-point inspection looks at the condition of your roof, electrical, plumbing, and HVAC systems to determine insurance eligibility. A wind mitigation inspection is only about wind resistance, and its goal is to lower what you pay, not to determine whether you can get covered at all.

A Note on the 2026 Form Update

The OIR-B1-1802 form was updated effective April 1, 2026. The new version reflects findings from a 2024 wind-loss study and updates the qualifying criteria and discount tables.

Reports completed before April 1, 2026, remain valid through their five-year window, but all new inspections now use the updated form. When scheduling, confirm your inspector is up to date on the new requirements.

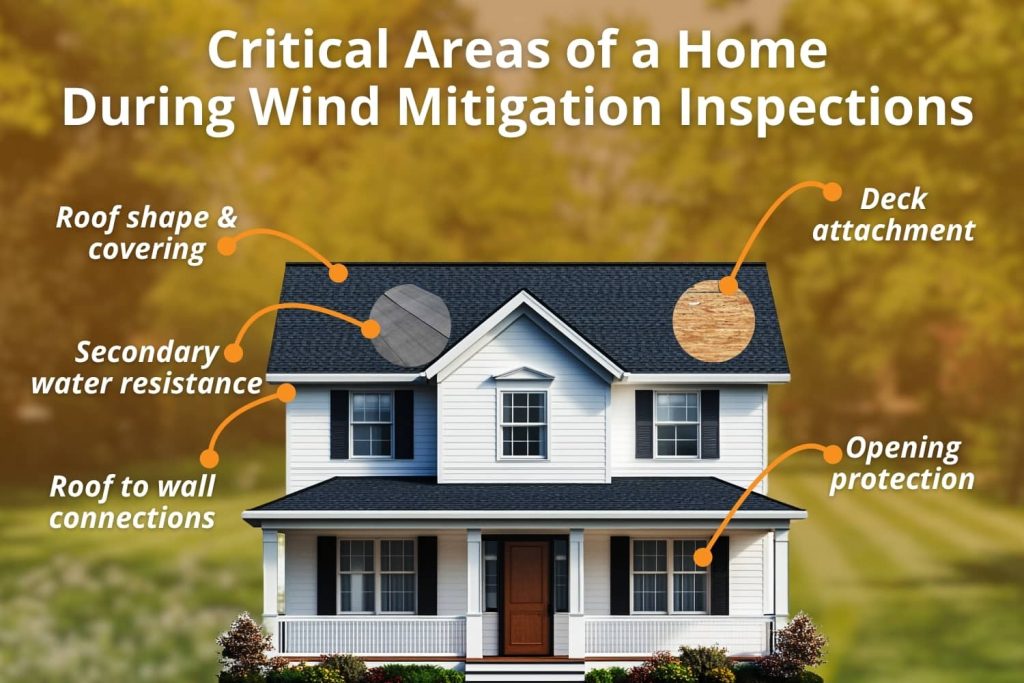

What Does a Wind Mitigation Inspection Look For?

The OIR-B1-1802 form covers seven specific construction features. Each one affects how much of a discount your insurer can apply.

1. Building Compliance

The inspector documents when the home was permitted and built. That date determines which version of the Florida Building Code was in effect at construction.

Homes built after 2001 fall under stricter wind-resistance standards, and newer construction generally earns larger credits for wind mitigation.

It’s important to know that this is a date verification, not a code compliance inspection.

2. Roof Covering

The type of roofing material and the date of the last roof replacement are documented. This tells the insurer how current and code-compliant the roof covering is.

3. Roof Deck Attachment

This is how the plywood or OSB panels underneath your shingles or tiles are nailed to the roof framing. Tighter nail patterns and larger nails provide better resistance to the roof lifting off. Homes with stronger deck attachment earn more credit.

4. Roof-to-Wall Attachment

This looks at how the roof trusses connect to the exterior walls. Options range from basic toenails (the weakest) to clips, single wraps, and double wraps (the strongest). Double-wrap hurricane straps offer the best protection and earn the highest credit in this category.

5. Roof Shape

Hip roofs, which slope on all four sides, perform much better in high winds than gable roofs, which have flat triangular ends. Hip roofs can experience up to 40% lower wind pressure at the same wind speed.

If your home in Orlando, Clermont, or Kissimmee has a hip roof, that’s likely one of your biggest credits.

6. Secondary Water Resistance (SWR)

This is a self-adhering membrane applied directly to the roof sheathing under the roof covering. It’s designed to keep water out if shingles are blown off during a storm.

Standard felt underlayment doesn’t qualify. When present and documented, SWR earns a solid credit and is common on roofs replaced in the last decade.

7. Opening Protection

This covers how well your windows, doors, skylights, and garage doors are protected from windborne debris. Impact-rated windows and doors, documented storm shutters, and reinforced garage doors all earn credits.

This is also the most all-or-nothing category: if even one opening lacks qualifying protection, the whole structure may receive no opening protection credit at all.

How Much Can You Save?

Savings vary based on which features your home has and which insurer you’re with. Florida law allows discounts of up to 88% off the windstorm portion of your policy, though the real-world impact for most Central Florida homeowners is more modest than that ceiling.

Homes that score well across multiple categories, especially hip roof geometry, double-wrap straps, SWR, and full opening protection, tend to see the largest premium reductions. A home without many of those features may still earn something in the building code compliance category, particularly if it was built after 2001.

Most homeowners recoup the inspection cost within the first few months of a new or renewed policy. Since the report is valid for up to five years, the savings extend well beyond year one.

Who Should Get One?

| Situation | Why It’s Worth It |

| You’ve never had one | You may be leaving discounts unclaimed on every renewal |

| You recently replaced your roof | New roofs often add SWR and stronger deck attachment |

| You added impact windows or shutters | Opening protection upgrades can unlock new credits |

| You’re buying a home | A current report clarifies insurance costs before closing |

| Your report is over five years old | Credits may have improved since your last inspection |

| You’re selling a home | A current report can be a selling point for insurance-aware buyers |

For buyers especially: in the Orlando metro and surrounding areas, insurance costs have a real impact on the total cost of owning a home.

Having a current wind mitigation report before closing gives you and your agent a clearer picture of what to expect.

What Happens After the Inspection?

Once the inspection is done, your inspector provides the completed OIR-B1-1802 form with photos documenting each credited feature. You submit that to your insurance agent or carrier, who applies the appropriate discounts to your policy.

Keep a copy of the report. It’s valid for up to five years, and if you switch carriers in that window, you can typically submit the same report to your new insurer without scheduling a new one. If you make significant upgrades like a new roof or impact windows, a fresh inspection can capture those improvements and potentially increase your credits.

One important note: Florida insurers won’t accept forms completed by an inspector whose license can’t be verified. An invalid form can cost you your discounts entirely, which is why choosing a licensed, trusted inspector matters.

Related Questions to Explore

What is a 4-point inspection, and how is it different from wind mitigation? A 4-point inspection evaluates the condition of a home’s roof, electrical, plumbing, and HVAC systems. Insurers use it to decide whether they’ll cover an older home at all. Wind mitigation is about how wind-resistant the home is, and it’s used to calculate discounts on an existing policy. Many homeowners schedule both at the same time to save on trip costs.

Do new construction homes in Central Florida need a wind mitigation inspection? Yes, and new construction often earns strong credits because it’s built to current Florida Building Code standards, which require tighter roof connections, stronger deck attachment, and better opening protection than older codes. Scheduling a new construction inspection lets you start claiming those credits right away.

What does a pre-listing inspection cover, and how can it help sellers? A pre-listing inspection is a full home inspection done before a property hits the market. It gives sellers a clear picture of the home’s condition and helps avoid surprises during a buyer’s inspection that could slow down or kill a contract. In Central Florida, pairing it with a current wind mitigation report is a strong combination, since buyers here are very aware of what insurance is going to cost them.

What is a sewer scope inspection, and when should you get one? A sewer scope uses a camera to inspect the main sewer line from the house to the street. It’s a good idea when buying older homes, homes with large trees near the sewer line, or any property with a history of slow drains or backups. It’s a quick add-on that can catch serious issues before they become your problem after closing.

When to Call a Professional

If you own a home in the Orlando area or anywhere in Central Florida and haven’t had a wind mitigation inspection in the last five years, it’s worth scheduling one.

The same goes if you’ve recently replaced your roof, added impact windows, or had hurricane straps installed. Each of those upgrades has the potential to earn credits that your current policy may not reflect.

For buyers, adding a wind mitigation inspection to your general home inspection visit is a practical step before closing.

Knowing your home’s wind-resistant features and what they could mean for your annual premium is part of making a smart purchase in a state where insurance costs aren’t something you can ignore.

Conclusion

A wind mitigation inspection is one of the few things a Florida homeowner can do that pays off quickly and keeps paying off for years. It’s fast, affordable, and the report can follow your home through multiple insurance policies. Whether you’re buying, selling, or just overdue for an updated report, the information it delivers is worth having.

At Central Florida Building Inspectors, we perform wind mitigation inspections throughout the Orlando metro and surrounding Central Florida communities, along with full home inspections, 4-point inspections, mold and air quality testing, and a full range of residential and commercial inspection services.

Reach out or schedule your inspection today.